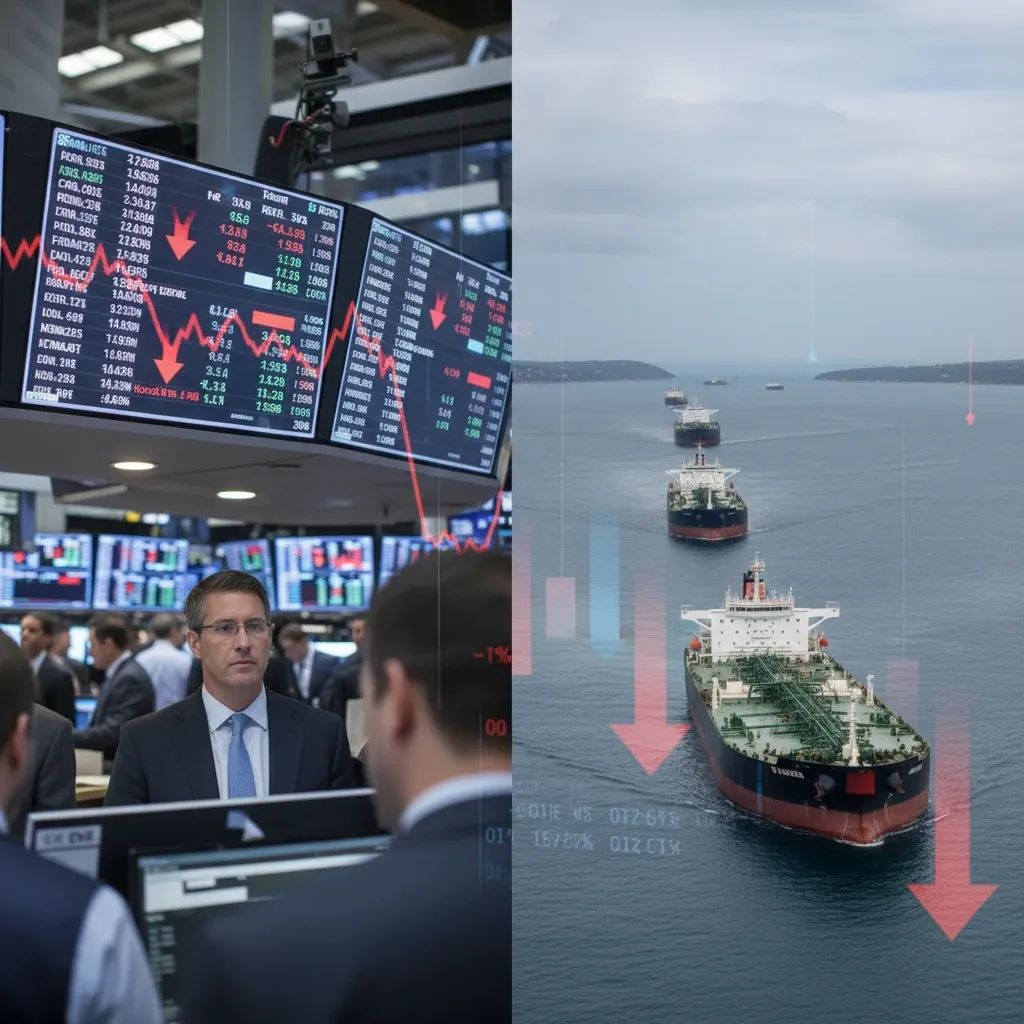

European equity markets closed lower on Monday as escalating U.S.-Iran confrontations in the Strait of Hormuz triggered renewed concerns over energy security and global trade routes. The Milan Stock Exchange finished marginally positive at +0.06%, buoyed by energy majors Saipem and ENI, while broader European indices slipped into negative territory amid ongoing geopolitical tensions over the critical maritime chokepoint.

Why This Matters

• Energy Exposure: Italian energy firms like ENI (+1.5%) and Saipem (+2.66%) rallied on oil price gains, offering short-term gains for investors with exposure to the sector.

• Inflation Risk: Brent crude climbed 1% to $72.70 per barrel, while natural gas surged 3.6% to €42.30 per megawatt-hour—pressures that could feed into household energy bills and industrial costs across Italy.

• Market Volatility: The FTSE MIB remains vulnerable to further disruptions, with geopolitical risk now a primary driver of near-term price movements.

• Negotiations Ongoing: International efforts are underway to de-escalate tensions and stabilize the Strait of Hormuz, though the outcome remains uncertain.

What Happened Over the Weekend

The latest round of U.S.-Iran hostilities continued over the weekend, with each side conducting strikes against the other. This escalation marks a significant deterioration in an already tense relationship and raises fresh concerns about potential disruptions to global energy supplies and maritime traffic through one of the world's most critical shipping lanes.

Following these attacks, Iran and Oman are engaging in preliminary discussions on how to manage shipping traffic through the Strait of Hormuz. Such coordination between nations bordering the strait could prove crucial in preventing further escalation and maintaining minimal levels of commercial navigation.

Italy's Energy Sector in Focus

The Milan bourse diverged from its European peers, finishing the session up 0.06% as Italian energy stocks absorbed the bulk of investor interest. Saipem, the oil services giant, surged 2.66%, while ENI, Italy's state-controlled energy major, gained 1.5% as West Texas Intermediate crude rose 1.4% to $70.20 per barrel.

Natural gas prices also spiked, climbing 3.6% to €42.30 per megawatt-hour on the Dutch TTF benchmark—the pricing reference for much of Europe. Italy imports a significant portion of its liquefied natural gas through routes that pass by the Strait of Hormuz. Any prolonged disruption to shipping in the region would increase energy costs for Italian households and businesses, potentially driving up inflation and straining consumer budgets.

The energy sector has been one of the few bright spots for European equity investors during periods of geopolitical tension. However, the broader picture is mixed: while upstream producers benefit from elevated commodity prices, downstream industries—particularly chemicals, manufacturing, and transportation—face margin pressure as input costs rise.

Impact on Italian Investors and Households

Beyond the stock market, the Hormuz tensions carry tangible consequences for Italian households and businesses. Elevated energy prices feed directly into inflation, potentially complicating monetary policy decisions. Economic forecasts have warned that prolonged Middle East tensions and persistent energy disruptions could slow European growth and reignite inflationary pressures.

For Italian companies dependent on global supply chains, shipping route disruptions add logistical strain. Vessels potentially rerouted around longer passages would face extended transit times, affecting industries reliant on timely delivery of components and raw materials.

Investors holding real estate and industrial stocks saw losses on Monday, reflecting broader concerns about economic slowdown and cost pressures. The real estate sector, in particular, remains sensitive to interest rate volatility, and any sustained inflation shock could affect borrowing costs and investment decisions.

Broader European Market Performance

While Milan managed a slim gain, other major European bourses closed in the red. Frankfurt's DAX fell 0.18% to 24,626 points, Paris's CAC 40 dropped 0.21% to 8,367 points, and London's FTSE 100 shed 0.23% to 10,484 points. The pan-European STOXX 600 index inched up nearly a quarter of a point, supported by gains in energy and technology stocks, though losses in real estate and industrials weighed on the broader index.

The Italian 10-year government bond yield held steady at 3.58%, while the spread between Italian BTPs and German Bunds remained relatively calm at 73.4 basis points—suggesting that for now, debt markets view the current tensions as a near-term challenge rather than a fundamental threat to European fiscal stability.

Currency markets reflected a modest flight to safety, with the euro showing slight movements. Precious metals showed mixed performance: gold remained relatively flat, while silver posted modest gains.

What Comes Next

International diplomatic efforts continue as nations seek to prevent further escalation and maintain open shipping lanes through the Strait of Hormuz. The coordination between Iran and Oman on strait management represents a potential pathway toward stabilization, though negotiations are still in early stages.

For Italian investors, the near-term outlook depends on several factors: the success of diplomatic efforts to de-escalate tensions, the pace of normalization in shipping traffic through the strait, and the trajectory of oil and gas prices. Energy stocks may continue to benefit as long as commodity prices remain elevated, but sustained disruption poses broader risks to economic growth and corporate earnings across sectors.

The situation underscores the systemic vulnerability of European economies to global energy shocks. Even as the European Union works to diversify its energy sources away from traditional Middle Eastern suppliers, markets remain exposed to price volatility and supply disruptions originating from geopolitically sensitive regions.

As diplomatic efforts progress, the question for Italian households and investors is whether international negotiations can prevent prolonged disruptions to the Strait of Hormuz, or whether the region will remain a source of economic uncertainty in the months ahead.